Mazda 3 Insurance Rates

Enter your zip code below to view companies that have cheap auto insurance rates.

Michelle Robbins

Licensed Insurance Agent

Michelle Robbins has been a licensed insurance agent for over 13 years. Her career began in the real estate industry, supporting local realtors with Title Insurance. After several years, Michelle shifted to real estate home warranty insurance, where she managed a territory of over 100 miles of real estate professionals. Later, Agent Robbins obtained more licensing and experience serving families a...

Licensed Insurance Agent

UPDATED: Apr 19, 2024

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident car insurance decisions. Comparison shopping should be easy. We are not affiliated with any one car insurance provider and cannot guarantee quotes from any single provider.

Our insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance related. We update our site regularly, and all content is reviewed by auto insurance experts.

The average insurance prices for a Mazda 3 are $998 every 12 months for full coverage insurance. Comprehensive costs an estimated $152, collision costs $214, and liability costs $474. Liability-only coverage costs as little as $522 a year, with high-risk coverage costing around $2,154. Teens cost the most to insure at $4,054 a year or more.

Average premium for full coverage: $998

Policy rates broken down by type of insurance:

Rates are based on $500 deductible amounts, bodily injury liability limits of 30/60, and includes both medical and uninsured motorist insurance. Prices are averaged for all 50 states and for different 3 trim levels.

Price Range Variability

For a 40-year-old driver, Mazda 3 insurance rates go from the cheapest price of $522 for minimum levels of liability insurance to a much higher rate of $2,154 for a driver who has had serious violations or accidents.

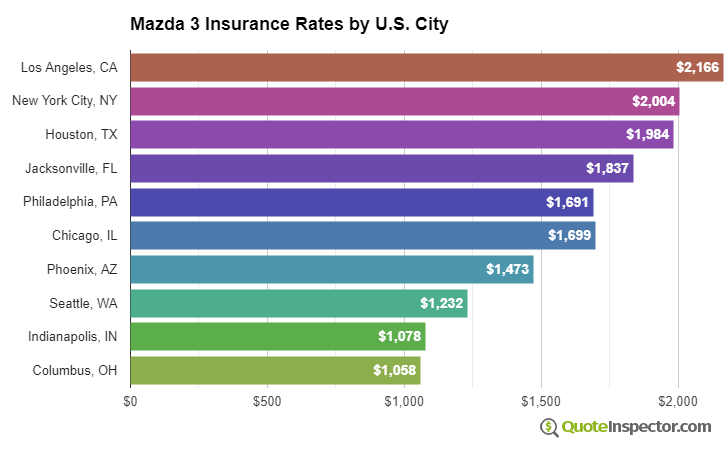

Urban vs. Rural Price Range

Your location can make a big difference on the price of insurance. More rural locations are shown to have more infrequent physical damage claims than cities with more traffic congestion.

The price range example below illustrates how your location can change insurance prices.

The examples above illustrate why anyone shopping for car insurance should compare rates for a targeted area and their own driving history, instead of making a decision based on averaged prices.

Use the form below to get customized rates for your location.

Enter your zip code below to view companies based on your location that have cheap auto insurance rates.

Additional Rate Details

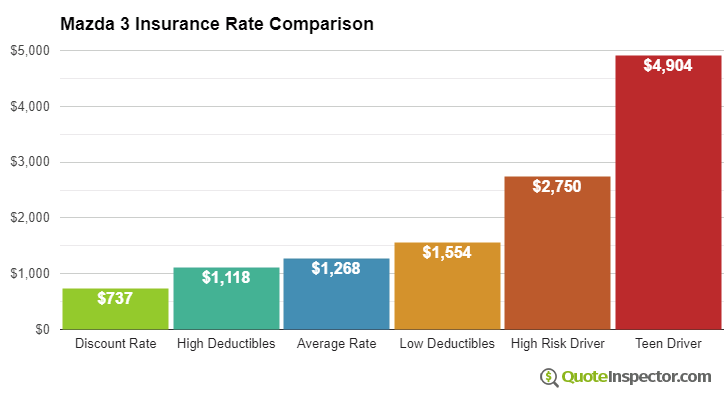

The chart below illustrates estimated Mazda 3 insurance rates for other coverage scenarios.

- The cheapest rate after discounts is $605

- Drivers who choose higher $1,000 deductibles will pay approximately $84 each year

- The average price for a good driver age 40 who has $500 deductibles is $998

- Selecting more expensive low deductibles for comprehensive and collision insurance increases the price to $1,158

- Drivers with serious driving violations could pay up to $2,154 or more

- Policy cost to insure a 16-year-old driver with full coverage can cost as much as $4,054 a year

Insurance rates for a Mazda 3 also range considerably based on liability limits and deductibles, your risk profile, and the model year and trim level.

Choosing higher comprehensive and collision insurance deductibles could save up to $250 annually, while increasing your policy's liability limits will increase premiums. Switching from a 50/100 liability limit to a 250/500 limit will raise rates by up to $426 more each year. View Rates by Deductible or Liability Limit

An older driver with no violations or accidents and higher deductibles may pay as low as $900 per year on average, or $75 per month, for full coverage. Rates are much higher for teenagers, since even excellent drivers should be prepared to pay at least $4,000 a year. View Rates by Age

If you have a few points on your driving record or you were responsible for an accident, you are probably paying $1,200 to $1,700 additional every year, depending on your age. High-risk driver insurance can cost from 42% to 134% more than the average policy. View High Risk Driver Rates

Your home state makes a big difference in Mazda 3 insurance prices. A 40-year-old driver could pay as low as $660 a year in states like North Carolina, Wisconsin, and Vermont, or have to pay at least $1,350 on average in Florida, New York, and Michigan.

| State | Premium | Compared to U.S. Avg | Percent Difference |

|---|---|---|---|

| Alabama | $904 | -$94 | -9.4% |

| Alaska | $766 | -$232 | -23.2% |

| Arizona | $828 | -$170 | -17.0% |

| Arkansas | $998 | -$0 | 0.0% |

| California | $1,138 | $140 | 14.0% |

| Colorado | $954 | -$44 | -4.4% |

| Connecticut | $1,026 | $28 | 2.8% |

| Delaware | $1,130 | $132 | 13.2% |

| Florida | $1,250 | $252 | 25.3% |

| Georgia | $922 | -$76 | -7.6% |

| Hawaii | $718 | -$280 | -28.1% |

| Idaho | $674 | -$324 | -32.5% |

| Illinois | $744 | -$254 | -25.5% |

| Indiana | $752 | -$246 | -24.6% |

| Iowa | $674 | -$324 | -32.5% |

| Kansas | $952 | -$46 | -4.6% |

| Kentucky | $1,362 | $364 | 36.5% |

| Louisiana | $1,476 | $478 | 47.9% |

| Maine | $616 | -$382 | -38.3% |

| Maryland | $822 | -$176 | -17.6% |

| Massachusetts | $798 | -$200 | -20.0% |

| Michigan | $1,736 | $738 | 73.9% |

| Minnesota | $834 | -$164 | -16.4% |

| Mississippi | $1,194 | $196 | 19.6% |

| Missouri | $886 | -$112 | -11.2% |

| Montana | $1,072 | $74 | 7.4% |

| Nebraska | $786 | -$212 | -21.2% |

| Nevada | $1,198 | $200 | 20.0% |

| New Hampshire | $718 | -$280 | -28.1% |

| New Jersey | $1,114 | $116 | 11.6% |

| New Mexico | $886 | -$112 | -11.2% |

| New York | $1,052 | $54 | 5.4% |

| North Carolina | $576 | -$422 | -42.3% |

| North Dakota | $818 | -$180 | -18.0% |

| Ohio | $690 | -$308 | -30.9% |

| Oklahoma | $1,026 | $28 | 2.8% |

| Oregon | $914 | -$84 | -8.4% |

| Pennsylvania | $954 | -$44 | -4.4% |

| Rhode Island | $1,332 | $334 | 33.5% |

| South Carolina | $904 | -$94 | -9.4% |

| South Dakota | $842 | -$156 | -15.6% |

| Tennessee | $876 | -$122 | -12.2% |

| Texas | $1,204 | $206 | 20.6% |

| Utah | $740 | -$258 | -25.9% |

| Vermont | $684 | -$314 | -31.5% |

| Virginia | $598 | -$400 | -40.1% |

| Washington | $774 | -$224 | -22.4% |

| West Virginia | $914 | -$84 | -8.4% |

| Wisconsin | $692 | -$306 | -30.7% |

| Wyoming | $890 | -$108 | -10.8% |

Because rates have so much variability, the only way to figure out which auto insurance is cheapest is to compare rates from multiple companies. Every company calculates rates differently, and rates will be varied.

Insurance Rates by Trim Level and Model Year

| Model and Trim | Annual Premium | Monthly Premium |

|---|---|---|

| Mazda 3 I Sport 4-Dr Sedan | $962 | $80 |

| Mazda 3 I SV 4-Dr Sedan | $962 | $80 |

| Mazda 3 I Touring 4-Dr Sedan | $998 | $83 |

| Mazda 3 S Sport 4-Dr Hatchback | $1,018 | $85 |

| Mazda 3 S Sport 4-Dr Sedan | $1,018 | $85 |

| Mazda 3 S Grand Touring 4-Dr Hatchback | $1,036 | $86 |

| Mazda 3 S Grand Touring 4-Dr Sedan | $1,036 | $86 |

Rates assume 2011 model year, a 40-year-old male driver with no accidents or violations, $500 comprehensive and collision deductibles, minimum liability limits, and uninsured/under-insured motorist coverage included. Rates are for comparison only and are averaged for all 50 U.S. states.

| Model Year | Comprehensive | Collision | Liability | Total Premium |

|---|---|---|---|---|

| 2024 Mazda 3 | $282 | $536 | $398 | $1,374 |

| 2023 Mazda 3 | $272 | $524 | $416 | $1,370 |

| 2022 Mazda 3 | $262 | $502 | $430 | $1,352 |

| 2021 Mazda 3 | $248 | $484 | $442 | $1,332 |

| 2020 Mazda 3 | $238 | $450 | $452 | $1,298 |

| 2019 Mazda 3 | $230 | $424 | $456 | $1,268 |

| 2018 Mazda 3 | $220 | $380 | $460 | $1,218 |

| 2017 Mazda 3 | $206 | $350 | $460 | $1,174 |

| 2016 Mazda 3 | $198 | $328 | $464 | $1,148 |

| 2015 Mazda 3 | $194 | $306 | $474 | $1,132 |

| 2014 Mazda 3 | $180 | $284 | $474 | $1,096 |

| 2012 Mazda 3 | $162 | $236 | $474 | $1,030 |

| 2011 Mazda 3 | $152 | $214 | $474 | $998 |

| 2010 Mazda 3 | $148 | $192 | $468 | $966 |

Rates are averaged for all Mazda 3 models and trim levels. Rates assume a 40-year-old male driver, full coverage with $500 deductibles, and a clean driving record.

How to Shop for the Best Cheap Mazda 3 Insurance

Finding cheaper rates on insurance for a Mazda 3 not only requires having a good driving record, but also having above-average credit, being claim-free, and maximizing policy discounts. Invest the time to shop around every other policy renewal by obtaining price quotes from direct insurance companies, and also from insurance agencies where you live.

The next list is a quick review of the ideas that were illustrated above.

- Drivers age 20 and younger are expensive to insure, possibly costing $338 each month if full coverage is included

- Drivers considered higher risk with a DUI or reckless driving violation could be forced to pay on average $1,160 more annually to buy Mazda 3 insurance

- Increasing comprehensive and collision deductibles could save as much as $250 each year

- It is possible to save approximately $110 per year simply by shopping early and online

Rate Tables and Charts

Rates by Driver Age

| Driver Age | Premium |

|---|---|

| 16 | $4,054 |

| 20 | $2,292 |

| 30 | $1,014 |

| 40 | $998 |

| 50 | $916 |

| 60 | $898 |

Full coverage, $500 deductibles

Rates by Deductible

| Deductible | Premium |

|---|---|

| $100 | $1,158 |

| $250 | $1,086 |

| $500 | $998 |

| $1,000 | $914 |

Full coverage, driver age 40

Rates by Liability Limit

| Liability Limit | Premium |

|---|---|

| 30/60 | $998 |

| 50/100 | $1,131 |

| 100/300 | $1,249 |

| 250/500 | $1,557 |

| 100 CSL | $1,178 |

| 300 CSL | $1,439 |

| 500 CSL | $1,629 |

Full coverage, driver age 40

Rates for High Risk Drivers

| Age | Premium |

|---|---|

| 16 | $5,706 |

| 20 | $3,656 |

| 30 | $2,168 |

| 40 | $2,154 |

| 50 | $2,060 |

| 60 | $2,038 |

Full coverage, $500 deductibles, two speeding tickets, and one at-fault accident

If a financial responsibility filing is required, the additional charge below may also apply.

Potential Rate Discounts

If you qualify for discounts, you may save the amounts shown below.

| Discount | Savings |

|---|---|

| Multi-policy | $50 |

| Multi-vehicle | $54 |

| Homeowner | $18 |

| 5-yr Accident Free | $61 |

| 5-yr Claim Free | $63 |

| Paid in Full/EFT | $36 |

| Advance Quote | $44 |

| Online Quote | $67 |

| Total Discounts | $393 |

Discounts are estimated and may not be available from every company or in every state.

Compare Rates and Save

Find companies with the cheapest rates in your area