Chevrolet Volt Insurance Rates

Enter your zip code below to view companies that have cheap auto insurance rates.

Michelle Robbins

Licensed Insurance Agent

Michelle Robbins has been a licensed insurance agent for over 13 years. Her career began in the real estate industry, supporting local realtors with Title Insurance. After several years, Michelle shifted to real estate home warranty insurance, where she managed a territory of over 100 miles of real estate professionals. Later, Agent Robbins obtained more licensing and experience serving families a...

Licensed Insurance Agent

UPDATED: Apr 20, 2024

It’s all about you. We want to help you make the right coverage choices.

Advertiser Disclosure: We strive to help you make confident car insurance decisions. Comparison shopping should be easy. We are not affiliated with any one car insurance provider and cannot guarantee quotes from any single provider.

Our insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about auto insurance. Our goal is to be an objective, third-party resource for everything auto insurance related. We update our site regularly, and all content is reviewed by auto insurance experts.

Car insurance can be expensive if you don’t know how to shop around for insurance. You may even think you already have a good rate, but a little shopping may reveal you could save hundreds more on car insurance. If you need to save on your Chevrolet Volt’s car insurance costs, you’ve come to the right place.

Our guide goes over rate changes by area, coverage, safety ratings, and much more, so you can understand how insurers calculate your rates and what to do to save money.

If you want to jump right into comparing average Chevrolet Volt car insurance rates, use our free rate tool by entering your ZIP code.

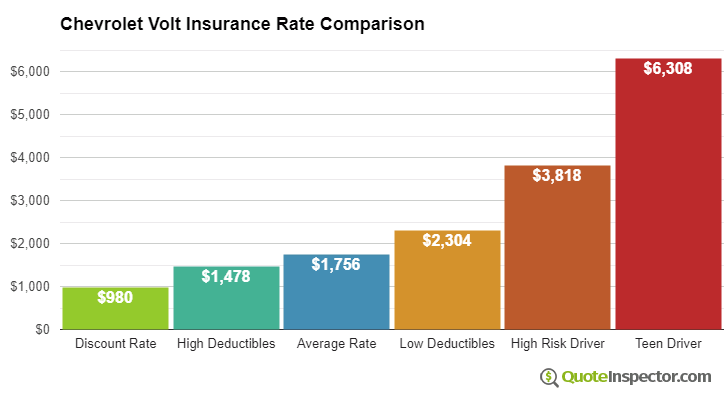

Average auto insurance rates for a Chevrolet Volt are $1,326 annually for full coverage. Comprehensive insurance costs around $254, collision insurance costs $440, and liability coverage is estimated at $474. A liability-only policy costs approximately $522 a year, and high-risk insurance costs $2,876 or more. Teen drivers receive the highest rates at up to $5,092 a year.

Average premium for full coverage: $1,326

Rate estimates for individual coverage type:

These estimates include $500 policy deductibles, 30/60 bodily injury liability limits, and includes medical/PIP and uninsured motorist coverage. Rates are averaged for all states and for different Volt trim levels.

Price Range by Coverage and Risk

For a driver around age 40, prices range range from as cheap as $522 for liability-only coverage to a much higher rate of $2,876 for a driver who requires high-risk insurance.

Price Range by Location

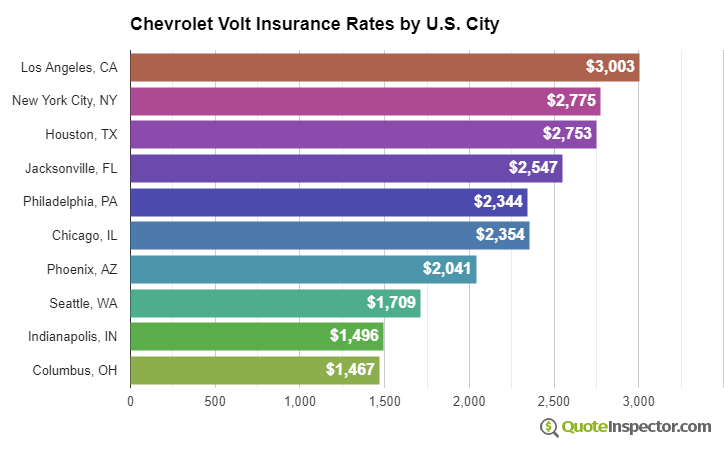

Living in a larger city has a large influence on auto insurance rates. Areas with sparse population tend to have fewer accident claims than larger metro areas. The price range example below illustrates the difference between rural and urban areas on auto insurance rates.

These examples show why anyone shopping for car insurance should get quotes for a specific zip code and their own personal driving habits, rather than using price averages.

Use the form below to get customized rates for your location.

Enter your zip code below to view companies based on your location that have cheap auto insurance rates.

Additional Charts and Tables

The chart below shows average Chevrolet Volt insurance rates for additional coverage choices and driver risks.

- The lowest rate with discounts is $771

- Choosing higher $1,000 deductibles can save about $158 a year

- The estimated rate for a 40-year-old driver using $500 deductibles is $1,326

- Choosing more expensive low deductibles for comp and collision coverage costs an additional $306 each year

- Drivers with multiple violations and an at-fault accident could pay at least $2,876

- The cost with full coverage for a teenage driver with full coverage can be $5,092 each year

Insurance rates for a Chevrolet Volt can also vary considerably based on the trim level of your Volt, your driver profile, and deductibles and policy limits.

An older driver with a clean driving record and high physical damage deductibles may only pay around $1,200 annually on average for full coverage. Rates are highest for teen drivers, where even without any violations or accidents they can expect to pay as much as $5,000 a year. View Rates by Age

If you like to drive fast or you caused a few accidents, you could be paying at least $1,600 to $2,200 extra per year, depending on your age. High-risk driver insurance ranges around 43% to 134% more than average. View High Risk Driver Rates

Choosing high deductibles can save as much as $470 a year, while increasing your policy's liability limits will increase rates. Going from a 50/100 bodily injury limit to a 250/500 limit will cost as much as $426 more per year. View Rates by Deductible or Liability Limit

Where you live plays a big part in determining prices for Chevrolet Volt insurance rates. A good driver about age 40 could pay as low as $870 a year in states like Idaho, Maine, and Iowa, or as much as $1,890 on average in Michigan, Louisiana, and New York.

| State | Premium | Compared to U.S. Avg | Percent Difference |

|---|---|---|---|

| Alabama | $1,200 | -$126 | -9.5% |

| Alaska | $1,016 | -$310 | -23.4% |

| Arizona | $1,100 | -$226 | -17.0% |

| Arkansas | $1,326 | -$0 | 0.0% |

| California | $1,510 | $184 | 13.9% |

| Colorado | $1,266 | -$60 | -4.5% |

| Connecticut | $1,362 | $36 | 2.7% |

| Delaware | $1,500 | $174 | 13.1% |

| Florida | $1,658 | $332 | 25.0% |

| Georgia | $1,224 | -$102 | -7.7% |

| Hawaii | $952 | -$374 | -28.2% |

| Idaho | $896 | -$430 | -32.4% |

| Illinois | $986 | -$340 | -25.6% |

| Indiana | $998 | -$328 | -24.7% |

| Iowa | $896 | -$430 | -32.4% |

| Kansas | $1,260 | -$66 | -5.0% |

| Kentucky | $1,810 | $484 | 36.5% |

| Louisiana | $1,962 | $636 | 48.0% |

| Maine | $818 | -$508 | -38.3% |

| Maryland | $1,094 | -$232 | -17.5% |

| Massachusetts | $1,060 | -$266 | -20.1% |

| Michigan | $2,304 | $978 | 73.8% |

| Minnesota | $1,108 | -$218 | -16.4% |

| Mississippi | $1,588 | $262 | 19.8% |

| Missouri | $1,178 | -$148 | -11.2% |

| Montana | $1,424 | $98 | 7.4% |

| Nebraska | $1,046 | -$280 | -21.1% |

| Nevada | $1,590 | $264 | 19.9% |

| New Hampshire | $954 | -$372 | -28.1% |

| New Jersey | $1,482 | $156 | 11.8% |

| New Mexico | $1,174 | -$152 | -11.5% |

| New York | $1,396 | $70 | 5.3% |

| North Carolina | $764 | -$562 | -42.4% |

| North Dakota | $1,086 | -$240 | -18.1% |

| Ohio | $914 | -$412 | -31.1% |

| Oklahoma | $1,362 | $36 | 2.7% |

| Oregon | $1,214 | -$112 | -8.4% |

| Pennsylvania | $1,266 | -$60 | -4.5% |

| Rhode Island | $1,768 | $442 | 33.3% |

| South Carolina | $1,202 | -$124 | -9.4% |

| South Dakota | $1,120 | -$206 | -15.5% |

| Tennessee | $1,162 | -$164 | -12.4% |

| Texas | $1,598 | $272 | 20.5% |

| Utah | $982 | -$344 | -25.9% |

| Vermont | $910 | -$416 | -31.4% |

| Virginia | $794 | -$532 | -40.1% |

| Washington | $1,026 | -$300 | -22.6% |

| West Virginia | $1,214 | -$112 | -8.4% |

| Wisconsin | $918 | -$408 | -30.8% |

| Wyoming | $1,182 | -$144 | -10.9% |

| Model Year | Comprehensive | Collision | Liability | Total Premium |

|---|---|---|---|---|

| 2019 Chevrolet Volt | $312 | $648 | $452 | $1,570 |

| 2018 Chevrolet Volt | $300 | $610 | $456 | $1,524 |

| 2017 Chevrolet Volt | $288 | $548 | $460 | $1,454 |

| 2016 Chevrolet Volt | $270 | $504 | $460 | $1,392 |

| 2015 Chevrolet Volt | $260 | $472 | $464 | $1,354 |

| 2014 Chevrolet Volt | $254 | $440 | $474 | $1,326 |

| 2013 Chevrolet Volt | $234 | $410 | $474 | $1,276 |

| 2012 Chevrolet Volt | $228 | $372 | $478 | $1,236 |

| 2011 Chevrolet Volt | $212 | $340 | $474 | $1,184 |

Rates are averaged for all Chevrolet Volt models and trim levels. Rates assume a 40-year-old male driver, full coverage with $500 deductibles, and a clean driving record.

How to Buy Cheap Chevrolet Volt Insurance

Saving money on auto insurance takes avoiding accidents and claims, having a good credit history, eliminating unneeded coverage, and dropping full coverage on older vehicles. Set aside time to compare rates at every other renewal by requesting rates from direct carriers like Progressive and GEICO, and also from local independent and exclusive agents.

The points below are a brief summary of the concepts that were covered above.

- Drivers that tend to have accidents or serious violations pay an average of $1,550 more every year to insure a Chevrolet Volt

- Drivers under the age of 20 pay higher rates, costing as high as $424 per month including comprehensive and collision insurance

- Drivers can save up to $160 per year just by shopping early and online

- Increasing deductibles could save up to $475 each year

- Drivers can save up to $160 per year just by shopping early and online

Just by getting quotes, you can save over $200 a year.

Free Car Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

How does the size and class of the Chevrolet Volt affect liability rates?

What does liability insurance cover? Required in most states, this coverage will protect you if you hit another driver by paying for the other driver’s medical bills and property damage costs. Insurers will raise your rates if your vehicle is in a size class that is proven to cause significant damage to other vehicles.

To help you understand how the size and class function in crashes, watch the crash test between a large SUV and a small car.

With liability insurance, it is not how your car fares in a crash that matters to insurers but how other cars will fare around your vehicle. This is why if your car is also shown to be likely to crash (perhaps there is a defect in the car or the car simply has a powerful engine encouraging speeding), insurers will raise your rates.

Because the Chevrolet Volt is a small, four-door car, it likely won’t do much damage to other cars. So unless it is prone to crashing, the liability rates shouldn’t be too bad. To make sure of this, however, we are going to take a look at the Insurance Institute for Highway Safety’s (IIHS) data on insurance losses by vehicle make and model.

- Bodily injury liability loss: -6 percent (average)

- Property damage liability loss: -12 percent (average)

Even though the Chevrolet Volt’s liability losses are average for its size group, the losses are still negative, which is great. Based on these losses, we can assume that the Chevrolet Volt has average insurance rates for liability coverage. To make sure, however, we are going to go over rates in the next section.

What does liability insurance cost for the Chevrolet Volt?

We went ahead and got a sample quote from Geico to show you how much liability insurance will cost and how it can change as you increase your coverage level. Our quote is based on a 40-year-old male driver in Pennsylvania who owns a 2019 Chevrolet Volt, has a bachelor’s degree, travels 13,000 miles a year, and has a clean driving record. Let’s start with the average rates for six months of bodily injury coverage.

- Low ($15,000/$30,000): $40.67

- Medium ($100,000/$200,000): $83.37

- High ($500,000/$500,000): $134.21

It will cost you an average of $43 to upgrade to medium coverage and $94 to upgrade to high coverage. This breaks down to $7 a month or $15 a month. The next set of rates is for property damage liability coverage.

- Low ($5,000): $436.93

- Medium ($20,000): $466.16

- High ($100,000): $487.53

The costs for upgrades for property damage liability coverage are low. It is only $30 more for medium coverage (or $5 a month) and $51 for high coverage (or $8 a month). This means that for both bodily injury and property damage liability, you will pay $12 more a month for medium coverage and $23 more a month for high coverage.

Broken down like this, the costs don’t seem as bad. We highly recommend purchasing at least medium coverage for your vehicle. Not having a high limit of liable coverage leaves you vulnerable to out of pocket costs and legal action.

What are the safety features and ratings of the Chevrolet Volt?

Car manufacturers have come a long way since they produced the first cars, which often didn’t even include seat belts. Today, the importance of safety features is emphasized by car manufacturers, and you should take note of them. The more safety features your car has, the cheaper your insurance rate will be.

AutoBlog.com found that the 2019 Chevrolet Volt has the following standard safety features:

- Crash prevention features include anti-lock brakes and stability control.

- Crash safety features include front-impact airbags, side-impact airbags, overhead airbags, knee airbags, and seatbelt pretensioners.

- Anti-theft protection features include vehicle intrusion alarm and ignition disable device.

The Chevrolet Volt’s multiple airbags offer more protection, which is important as the Chevrolet is a smaller vehicle. However, the base model’s feature list is missing anti-whiplash headrests, which can help prevent neck injuries in a crash. Still, overhead airbags should help protect passengers in case of a rollover.

In addition to safety feature discounts, the crash rating of your vehicle model can help reduce your rates. The IIHS performed crashworthiness tests on the 2015 Chevrolet Volt sedan and hatchback models. Let’s take a look at how these two versions fared.

- Small overlap front (driver-side) crash test: Good (hatchback) and Acceptable (sedan).

- Moderate overlap front: Good (hatchback) and Good (sedan).

- Side: Good (hatchback) and Good (sedan).

- Roof strength: Good (hatchback) and Good (sedan).

- Head restraints and seats: Good (hatchback) and Good (sedan).

Both versions of the 2015 Chevrolet Volt did well, as good is the highest rating and acceptable is the second-highest rating. Because the Chevrolet Volt has such great crashworthiness tests, you should have a lower rate, especially if you have the sedan version (the IIHS awarded the 2015 Chevrolet sedan the top safety pick award for 2015).

However, cars do have more fatalities than SUVs and pickups, so rates may still be a little higher. The IIHS’s 2018 data on driver fatalities per million vehicles recorded the following fatalities: 48 car fatalities, 34 pickup fatalities, and 23 SUV fatalities. For all occupant fatalities, the numbers are as follows: 69 car fatalities, 42 pickup fatalities, and 32 SUV deaths.

The IIHS’s data suggests that pickups and SUVs are safer than cars. However, a more extensive study on crash performance would have to be done to make certain. There is some data on fatalities by crash types for cars, which we’ve included below.

- Frontal Impact: 7,433 fatalities

- Side Impact: 3,568 fatalities

- Rear Impact: 834 fatalities

- Other (mostly rollovers): 1,303 fatalities

There were a total of 13,138 fatalities for cars in 2018, which is very high. To put this number in perspective, in 2018, there were a total of 4,369 pickup fatalities and 5,035 SUV fatalities. Still, the great crash ratings of the Chevrolet Volt will balance out the negativity of higher fatality rates for cars, so you should still get a decent rate.

What is the MSRP of the Chevrolet Volt?

MSRP is an acronym for the manufacturer suggested retail price. This is the value a manufacturer believes its car is worth. Sellers will use the MSRP to create their invoice price, also known as the sticker price. Few people will pay the sticker price or the MSRP price.

Instead, shoppers will often purchase a car at what is known as the fair market price. This is the price you should be looking for when you shop for a vehicle. Watch the video below for a further explanation of these car prices.

Below, you can see Kelley Blue Book’s (KBB) price estimates for a 2019 Chevrolet Volt.

- MSRP: $34,395

- Invoice: $33,121

- Fair Market Range: $30,264 to $33,295

- Fair Purchase Price: $31,780

The fair purchase price is significantly lower than the MSRP and invoice prices. However, insurers don’t really care about the fair purchase price. The price that insurers use to calculate your collision and comprehensive car insurance rates is the MSRP.

The MSRP gives insurers an idea of how much parts will cost for repairs or how much it will cost to replace your car if you total it. If insurers don’t calculate rates properly, they risk a financial loss if you file a claim. This is also why lenders sometimes force people to buy comprehensive and collision car insurance when they sign the car lease.

If lenders don’t use force-placed insurance, they have no guarantee that drivers will carry collision and comprehensive coverage. These two coverages are what protect your lender from financial loss if you are in any of the following types of crashes:

- Collision coverage covers repair costs if you collide with another vehicle or an object like a fence post.

- Comprehensive coverage covers repair costs if natural disasters or bad weather wreck your vehicle. It will also cover damage from animal collisions, vandalism, and theft.

Both lenders and insurers will use the loss history (claims paid) on your vehicle to help determine rates for these two coverages. Insurers are well aware of what the best and worst vehicles are for overall collision losses. If your vehicle has poor losses, you will pay more.

While the IIHS listed great losses for comprehensive coverage, collision coverage losses were only average.

- Chevrolet Volt Collision Losses: -6 percent (average)

- Chevrolet Volt Comprehensive Losses: -32 percent (substantially better than average)

Since the Chevrolet Volt’s losses are decent, you shouldn’t have a very high rate for car insurance.

How much will it cost to repair my Chevrolet Volt?

If you have a deductible, you will have to pay for some of the repairs yourself until insurance steps in. For example, if you have a $500 deductible and are in an accident, you will have to pay $500 towards accident costs before your insurer will pay the rest. This is why it’s important to pick a deductible that you can pay.

Insurers, however, are concerned with the costs of repair, not what your deductible is. After all, your deductible is what you’ll have to pay. The costs of repair are what your insurer will have to pay to get you back on the road.

On RepairPal.com, the Chevrolet Volt’s alternative fuel average annual repair costs are estimated to be $550. This price estimate includes regular maintenance, such as inspections and oil changes. While the Chevrolet Volt’s average repair costs are less than repair costs for all vehicles ($652), it is still more expensive than repair costs for alternative fuel vehicles ($471).

Still, RepairPal.com gave the Chevrolet Volt a reliability rating of four out of five stars. This is great, as it means the Chevrolet Volt is more reliable than other vehicles. This means fewer breakdowns and unscheduled trips to the repair shop.

Our hope is that our guide to the Chevrolet Volt’s rates has given you the tools you need to find cheap car insurance. By understanding the basics of what determines the price of car insurance and shopping around, you can save hundreds every year. Want to start comparison shopping for Chevrolet Volt insurance costs right away? Use our free tool to start comparing rates.

Rate Tables and Charts

Rates by Driver Age

| Driver Age | Premium |

|---|---|

| 16 | $5,092 |

| 20 | $3,058 |

| 30 | $1,372 |

| 40 | $1,326 |

| 50 | $1,214 |

| 60 | $1,190 |

Full coverage, $500 deductibles

Rates by Deductible

| Deductible | Premium |

|---|---|

| $100 | $1,632 |

| $250 | $1,490 |

| $500 | $1,326 |

| $1,000 | $1,168 |

Full coverage, driver age 40

Rates by Liability Limit

| Liability Limit | Premium |

|---|---|

| 30/60 | $1,326 |

| 50/100 | $1,421 |

| 100/300 | $1,539 |

| 250/500 | $1,847 |

| 100 CSL | $1,468 |

| 300 CSL | $1,729 |

| 500 CSL | $1,919 |

Full coverage, driver age 40

Rates for High Risk Drivers

| Age | Premium |

|---|---|

| 16 | $7,244 |

| 20 | $4,882 |

| 30 | $2,926 |

| 40 | $2,876 |

| 50 | $2,746 |

| 60 | $2,720 |

Full coverage, $500 deductibles, two speeding tickets, and one at-fault accident

If a financial responsibility filing is required, the additional charge below may also apply.

Potential Rate Discounts

If you qualify for discounts, you may save the amounts shown below.

| Discount | Savings |

|---|---|

| Multi-policy | $70 |

| Multi-vehicle | $71 |

| Homeowner | $21 |

| 5-yr Accident Free | $93 |

| 5-yr Claim Free | $86 |

| Paid in Full/EFT | $57 |

| Advance Quote | $64 |

| Online Quote | $93 |

| Total Discounts | $555 |

Discounts are estimated and may not be available from every company or in every state.

Compare Rates and Save

Find companies with the cheapest rates in your area